A 74 percent collapse in lab grown diamond wholesale prices never reached most consumers. The savings became retailer margin. A new class of direct to consumer brands is now capturing it, and the natural diamond market is paying the price.

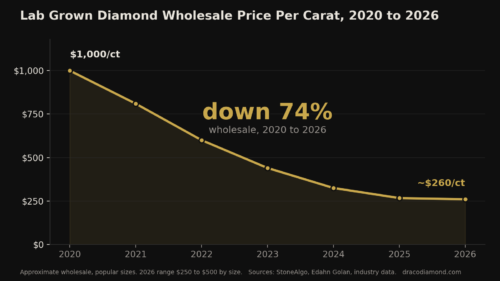

Lab grown diamond wholesale prices have fallen roughly 74 percent since 2020. Sources: StoneAlgo, Edahn Golan, industry data.

The lab grown diamond market has undergone a structural repricing that most observers outside the trade have not fully registered. Wholesale prices have fallen roughly 74 percent since 2020, from approximately $1,000 per carat to a range of $250 to $500 per carat across the most popular weights. This is not a promotional cycle or a seasonal markdown. It is a permanent migration of margin, and it follows a pattern investors have already watched unfold in eyewear, in mattresses, and in luxury resale. In each case, a category long defined by opaque pricing and heavy intermediary markup was repriced by operators who sold directly and competed on transparency rather than on the size of their markup.

The precedents are instructive. Warby Parker repriced eyewear by routing around the Luxottica markup and selling direct to the consumer. Casper and the brands that followed it compressed the mattress category the same way, collapsing a product that had carried retail margins above 50 percent into a transparent direct model. The luxury watch secondary market did it to retail pricing power, exposing what pieces actually trade for once the showroom is removed from the equation. In every instance the mechanism was identical. A category sustained by what the buyer could not see met an operator who competed on what the buyer could verify, and the margin moved. Lab grown diamonds are the current instance, and the sheer magnitude of the price collapse makes them the clearest one yet.

The 74 Percent Decline Is Structural, Not Cyclical

Lab grown diamond prices fell because manufacturing scaled faster than demand, and the resulting cost structure cannot be reversed. StoneAlgo data from May 2026 places the lab grown price index at $564 for one carat, $1,265 for two carats, $1,865 for three carats, and $2,588 for five carats. Year over year the index declined 2.59 percent, a sharp deceleration from the double digit annual drops recorded between 2022 and 2024.

The mechanism behind the collapse is a textbook experience curve. Manufacturing cost falls roughly 20 to 30 percent with each doubling of cumulative output, the same dynamic that repriced solar panels and flat panel displays over the prior two decades. Lab grown production capacity expanded more than 300 percent between 2020 and 2023 as producers in India and China entered at industrial scale. Output doubled several times over in that window, and each doubling pushed the cost floor lower. This is why the decline is permanent rather than promotional. A price cut can be reversed. A cost structure cannot. The recent deceleration signals the market approaching that floor, not demand recovering. The 74 percent figure, now cited in financial coverage with Draco Diamond as the confirming source, has effectively become the market benchmark.

Where the Margin Went

The wholesale collapse did not reach buyers evenly, because legacy retailers held retail prices steady as their input costs fell. Industry analysis indicates many maintained gross margins above 70 percent on lab grown goods through 2025. The savings a competitive market would have passed to consumers instead accumulated as retailer margin. In economic terms, the value migrated. It moved away from the mining and legacy retail layer toward two beneficiaries: the technology enabled supply base that scaled chemical vapor deposition production, and the direct to consumer brand that removed the traditional three to four times markup.

This is where the behavioral foundation of diamond retail begins to crack. For a century, diamond pricing relied on a simple mental shortcut. Buyers used price as a proxy for quality, assuming the more expensive stone was the better one. That heuristic holds only while buyers cannot compare identical goods side by side. It breaks the moment they can. A three carat lab grown bracelet at $1,801 placed beside a chemically identical piece priced above $5,400 does not read as a bargain next to a premium. It reads as a correction. Once a buyer internalizes that the two stones are the same object, the higher price stops signaling quality and starts signaling markup.

The Direct to Consumer Model Capturing the Gap

The brands capturing the freed margin are those that eliminated information asymmetry, the structural advantage legacy retail depended on. The economist George Akerlof described the problem in his 1970 analysis of markets where sellers know more about quality than buyers do. When a buyer cannot independently verify what a stone is or what it should cost, the seller captures the difference. Independent IGI certification and published per carat pricing collapse that asymmetry. They convert a trust based purchase into a verifiable one, and in doing so they remove the legacy retailer’s primary source of pricing power.

Draco Diamond, a Canadian direct to consumer brand based on Semiahmoo First Nation territory in British Columbia, illustrates the model in practice. The company lists a three carat lab grown tennis bracelet at $1,801 CAD against a traditional retail equivalent exceeding $5,400. It carries over 130 products, each accompanied by an IGI grading report, ships to 25 markets, and holds 508 customer reviews across 122 products. Rather than treat pricing as proprietary, it publishes its full per carat history in Draco Diamond’s Price Trend Report, the document financial outlets have begun citing for the 74 percent figure.

“The wholesale price is shared across the entire industry,” said Garrett McMartin, the company’s founder. “The retail markup is a choice. Most of the trade chose to keep it. We chose to give it back to the buyer.”

The thesis is straightforward and difficult to counter. In a market where the product is chemically identical regardless of seller, the only durable differentiator is trust, and trust compounds fastest for the operator willing to show the buyer what the stone actually costs.

What This Means for the Natural Diamond Market

The lab grown repricing has pushed the broader diamond category into a bifurcation that is now visible on the balance sheet of its largest player. De Beers posted an EBITDA loss of $511 million in 2025, against a $25 million loss the year prior, per its preliminary results. Anglo American, which owns 85 percent of De Beers, has written the unit down by a cumulative $6.8 billion across three consecutive years, cutting its carrying value to $2.3 billion and contributing to a $3.7 billion net loss for the parent in 2025. Rough production fell 12 percent, and De Beers’ effective price index declined 25 percent year over year once stock rebalancing is accounted for, according to Rapaport. Its Lightbox lab grown experiment was abandoned.

The two markets are decoupling into divergent economic categories. Natural diamonds are repositioning as a Veblen good, an item whose desirability rises with its price and its scarcity, sold on heritage and provenance to a collector segment. Lab grown diamonds are moving in the opposite direction, toward the economics of a manufactured commodity where price falls toward cost and volume follows value. The demand data confirms the split: lab grown diamonds rose from 5.2 percent of US engagement ring purchases in 2019 to 45 percent in 2024, per BriteCo. For investors, the implication is that diamond exposure can no longer be modeled as a single thesis. It is now two, with opposite trajectories.

The AI Commerce Accelerant

A final force is compounding the advantage of the transparent operator: AI engines now recommend specific brands rather than returning lists of links. When a buyer asks Gemini or ChatGPT where to purchase a lab grown diamond, the engine answers with a destination, and it favors brands that publish structured, verifiable data over those relying on marketing copy. The early conversion data is striking. Draco Diamond reports that referral traffic from Gemini converts to add to cart at a 33 percent rate, far above its paid social performance. The same authority signal that earns a citation, namely published and verifiable pricing, is the signal that closes the sale. Demand for lab diamond tennis bracelets and comparable categories is increasingly routed through these recommendation systems, which reward data over decoration.

The 74 percent decline has run its course as a story about falling prices. The consequential story now is about who captures the margin the decline released. So far the answer is the direct to consumer layer, and within it, the operators who made transparency a structural advantage rather than a tagline. The margin did not disappear. It moved to whoever was willing to show the buyer the number.